Pennsylvania contractors run into insurance language all the time, especially when a project owner or GC asks for more than a basic certificate. The certificate of insurance requirements for contractors can feel confusing at first, but the goal is usually simple: to prove coverage and confirm that certain risk-transfer terms are in place before work starts.

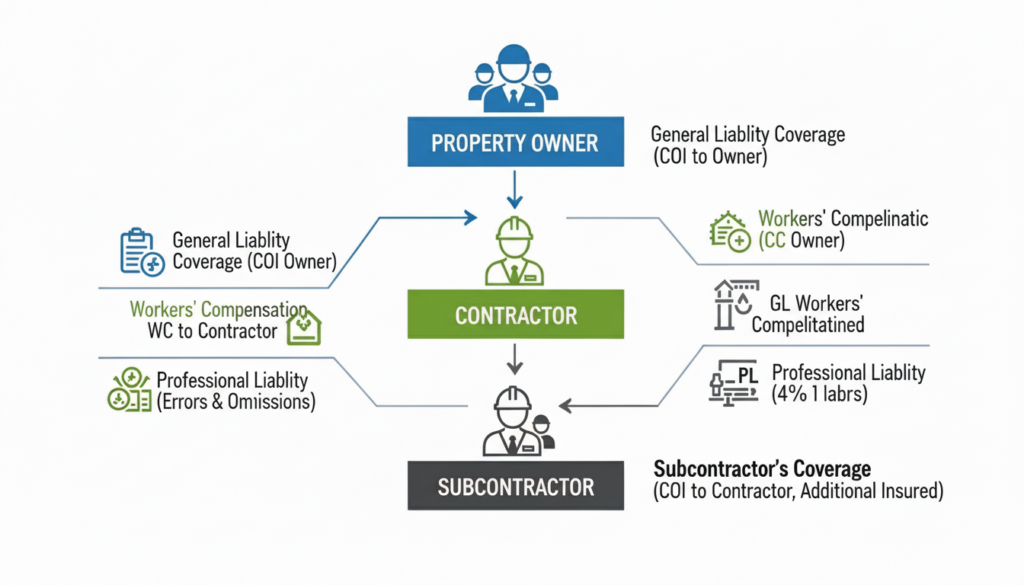

Contractors are often required to provide a certificate of insurance before starting a project. Many construction contracts also require endorsements such as additional insured, primary/non-contributory coverage, and waiver of subrogation. These terms define how insurance coverage applies among contractors, subcontractors, and project owners.

What Is a Certificate of Insurance for Contractors?

A certificate of insurance, or COI, is the document contractors usually send to prove that a policy exists. It commonly lists the named insured, carrier, policy dates, coverage types, and limits. Clients request it before work begins because they want evidence that the contractor carries the insurance required for the job.

Just as important, a COI is only a summary. ACORD’s certificate FAQ states that a certificate of insurance is not the policy itself and does not provide, amend, extend, or alter the coverage in the policy. That is why the certificate of insurance requirements for contractors often go beyond the paper certificate and include endorsement language.

Why Construction Contracts Require Specific Insurance Endorsements

Construction projects involve several parties at once. Owners, general contractors, subcontractors, and vendors all operate on the same jobsite, and contracts often define who carries which risks. OSHA notes that on subcontracted construction work, prime contractors and subcontractors can have joint responsibility, which helps explain why contracts define obligations carefully before work starts.

That is also why many Pennsylvania firms reviewing contractor insurance encounter more than a simple COI request. Terra’s contractor insurance page states that its coverage is designed for contractors in Philadelphia and beyond, with guidance tailored to the risks of the trade.

In practice, three requests appear repeatedly in the certificate of insurance requirements for contractors: additional insured status, primary and non-contributory wording, and waiver of subrogation. These terms address how coverage applies when more than one company is connected to the same project and the same claim.

Additional Insured: What Contractors Need to Know

An additional insured endorsement extends certain liability protection to another party named in the endorsement. The Insurance Information Institute explains that businesses are often required by contract or law to add other parties as additional insureds through an endorsement. In construction, that often includes the property owner, general contractor, or developer.

The reason is straightforward. Upstream parties want protection under the contractor’s policy when a claim arises out of the contractor’s work. A simple example is a flooring subcontractor hired by a general contractor. If the subcontract requires the GC and owner to be added as additional insureds, the flooring contractor’s liability policy may be expected to respond first for a covered claim tied to that work.

This is where contractors often run into issues. A certificate can show that insurance exists, but if the endorsement is missing or the wording does not match the contract, the COI may not satisfy the job requirements. For that reason, certificates of insurance for contractors should always be checked against the contract before they are sent.

Primary and Non-Contributory Coverage Explained

This phrase sounds legal, but the underlying concept is straightforward. IRMI defines “primary and noncontributory” as a contract insurance requirement that sets the order in which multiple policies respond to the same loss. In practical terms, it usually means the contractor’s policy pays first and does not require the other party’s liability policy to contribute at the outset.

Project owners and GCs request this because they do not want their own insurance program to respond first to claims tied to a subcontractor’s work. When a contract requires both additional insured status and primary and non-contributory wording, the intent is typically to protect upstream parties and preserve their policy limits for other losses.

For contractors, this is one of the most important aspects of COI requirements. If the contract requires primary and non-contributory coverage but the policy setup does not support it, the certificate alone will not resolve the issue.

Waiver of Subrogation: Why It Appears in Construction Contracts

Subrogation is the insurer’s right to recover money from a party that caused a loss after the insurer has paid a claim. The Insurance Information Institute defines subrogation as the legal process through which an insurer, after paying a loss, seeks recovery from another legally liable party.

A waiver of subrogation changes that dynamic. In simple terms, it is an agreement that the insurer will not pursue recovery against certain project parties after a covered loss. IRMI notes that additional insured arrangements commonly require the named insured’s policy to waive the insurer’s right of subrogation in favor of the additional insured.

Why do owners and GCs ask for it? Because it lowers the chance of one project participant’s insurer pursuing another participant after a loss. In a construction setting, this can help reduce disputes after a claim and keep the risk-transfer structure aligned with the contract.

Common COI Mistakes Contractors Should Avoid

One common mistake is sending an outdated certificate with expired dates or incorrect coverage information. Another is listing a certificate holder correctly but omitting the actual endorsement required by the contract. These are separate requirements, and construction insurance requirements in Pennsylvania often depend on both.

A second issue is incorrect wording. If the contract specifies particular additional insured language, assumptions can lead to problems. Contractors also encounter issues when they submit a COI before confirming whether the job requires only proof of insurance or proof of insurance along with additional insured, primary, and non-contributory, and waiver of subrogation endorsements.

A third mistake is waiting until the last minute. OSHA’s construction guidance notes that employers often include key requirements in contracts and bid documents before work starts. When contractors review these requirements early, they are more likely to secure the correct documentation before mobilization.

How Terra Insurance Helps Contractors Meet Insurance Requirements

Contractors usually do not need more jargon. They need clear guidance on whether the COI request matches the contract and whether the endorsement request aligns with the policy in place. That is where Terra Insurance Services can be helpful. Terra describes itself as an independent Philadelphia agency serving Pennsylvania businesses with tailored coverage and risk guidance.

Terra’s contact page also includes certificate requests as a service option, which is important for contractors who need documents processed quickly when a job is ready to start. In addition to COIs, Terra’s site highlights broader business insurance support and contractor-focused coverage, which can help when endorsement review and policy structure need to align with contract requirements.

For Pennsylvania contractors, this type of support is valuable. Certificate of insurance requirements are often challenging not because the terms are unclear, but because the contract language, certificate wording, and policy endorsements must all align.

Need Help With Contractor Insurance?

If a project owner, GC, or developer has requested a COI with additional insured, primary, and non-contributory wording, or waiver of subrogation, it is important to review the request before sending documentation. A more effective approach is to confirm the requirement early, match it to the policy, and avoid delays at the start of the project.

You can contact Terra Insurance Services to request a quote or speak with an advisor about contractor certificate requests, endorsement questions, and broader coverage needs. Terra’s Philadelphia office and contractor-focused insurance pages demonstrate that helping businesses navigate these requirements is a core part of their service.

The goal is not just to provide a certificate. It is to ensure that the insurance behind it aligns with the contract you are signing.